Financial

Vora Says Penn Destroyed $11 Billion in Value with Sour OSB Deals

Posted on: May 21, 2025, 05:25h.

Last updated on: May 22, 2025, 10:07h.

![]()

- Vora says Penn fumbled online gaming opportunity by focusing on sports betting

- Vora estimates Penn destroyed $11 billion in shareholder value with bad sports wagering transactions

- Calls Penn a sports betting “laggard”

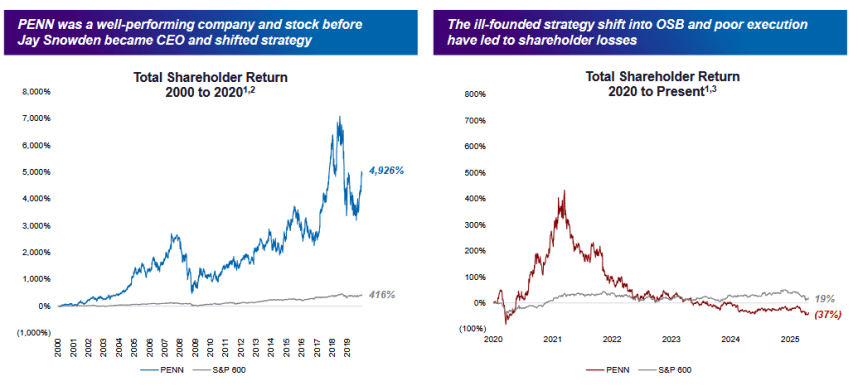

In its latest salvo aimed at Penn Entertainment (NASDAQ: PENN), HG Vora said the gaming company has destroyed $11 billion in shareholder value since 2021 by focusing on sports wagering, simultaneously fumbling opportunity to establish itself as a leader in the internet casino space.

In a presentation entitled “Genuine Change Is Needed At PENN,” the hedge fund notes that soon after David Handler became chairman of the board in 2019 and Jay Snowden became chief executive officer the following year, the gaming company set out to become an online sports betting (OSB) leader, resulting in a series of ill-fated transactions that plagued the stock price.

Shareholders have suffered greatly due to poor strategic decisions, failed transactions, and poor execution; absolute and relative total shareholder returns have been abysmal and more than $11 billion of shareholder value has been destroyed since 2021,” according to the hedge fund, which is attempting to place three hand-picked candidates on Penn’s board of directors.

The “failed transactions” to which Vora is referring are Penn paying more than $500 million to acquire Barstool Sports, doling out $2 billion in equity for theScore, and the August 2023 agreement with ESPN that could cost as much as $2 billion over a decade. Vora notes that on a combined basis, those deals equate to more than double Penn’s current market capitalization.

Penn Stock Has Languished Amid Sports Betting Focus

In a sentiment echoed by other investors, much of Vora’s dismay regarding Handler and Snowden’s leadership revolves around two points. First, Penn was a strong stock for two decades prior to the operator pushing into OSB. Second, that emphasis prompted investors to focus more on sports wagering than the operator’s profitable, though less glamorous, land-based regional casinos.

Indeed, Penn is in the midst of an unceremonious decline. Fifty months ago, the stock traded at around $140 and joined the S&P 500. As of Wednesday, the shares closed at $14.20 and the stock has since been removed from both the S&P 500 and S&P MidCap 400 Index, and was sent packing to the S&P SmallCap 600 Index.

Last week, HG Vora founder Parag Vora sent a letter to Penn shareholders in which he said “PENN trades at a discount to its intrinsic value because its management team and Board of Directors have lost credibility and investors fear further value-destructive decisions.” The money manager adds the gaming company’s board has indulged Snowden’s high compensation while shareholders have suffered.

“Paid the CEO near the top of the Company’s peer group despite consistent total shareholder return underperformance during his tenure; earned Say-on-Pay votes that were among the worst in the S&P 600,” according to the presentation.

Vora Not Buying Penn’s Claims

While there is some momentum for Penn’s standalone Hollywood Casino iGaming platform, Vora isn’t buying claims that the operator’s interactive unit “is nearing an inflection point.” The hedge fund points out that Penn has pushed the timeline for digital profitability out to 2026 from 2025, adding that ESPN Bet’s market share of roughly 2% is well below the operator’s long-term goal of 10%.

Average monthly active users of PENN’s Interactive products have declined by nearly 30% since the launch of ESPN Bet,” according to the investor. “PENN’s Interactive segment is still losing money, with its most recent quarterly Adjusted EBITDA loss bringing its cumulative Adjusted EBITDA losses since 2019 above $1 billion.”

Vora believes value can be created at Penn by refreshing the board with its three independent candidates, right-sizing executive compensation, introducing more challenging related benchmarks, and developing specific strategies for each component in the interactive unit.

Most Read

Most Read

Another Shooting Near Las Vegas Strip Casino Injures Man

Conversation (1 comment)